Section 21 of the IGST Act 2017 states that all services Imported on or after 1st July (appointed day) are liable to tax under GST, regardless of whether the transactions for such import of services had been initiated before the appointed day.

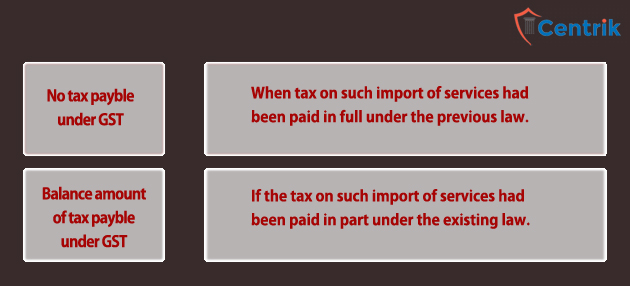

An exception to section 21 of the IGST Act, 2017 are as follows:

For the purposes of this section, a transaction shall be deemed to have been initiated before the appointed day if either the invoice relating to such supply or payment, either in full or in part, has been received or made before the appointed day.

According to section 7(l)(b) of CGST Act, 2017, import of services for a consideration whether or not in the course or furtherance of business, will be considered as supply.

Schedule I of CGST Act, 2017 states that Import of services by a taxable person from a related person or from any of his other establishments outside India, in the course or furtherance of business, made even without consideration will be treated as supply under GST.

Note – Please note that the above article is part of our continuous research on the related matters. It is based on our interpretation of related regulations which may differ person to person. Readers are expected to take expert opinion before relying on above.